Turn Idle Wealth into Tax-Efficient Income & Legacy

The Situation

Michael and Daniel are both 45 years old, successful professionals who have done everything “right” financially.

Their registered accounts are fully maxed out

They’ve accumulated $750,000 each in non-registered savings

They’re in a high tax bracket

They want to:

Supplement retirement income

Leave a meaningful inheritance

They can each comfortably allocate $30,000 per year for the next 20 years toward a long-term strategy.

The Challenge

Like many high-income earners, they faced a common problem:

“We’re saving well… but are we doing it efficiently?”

Their concerns:

Heavy tax drag on non-registered investments

Limited income efficiency in retirement

Desire to maximize estate value, not just accumulate assets

Two Different Approaches

Strategy 1 (Michael): Traditional Approach

$1M Term 20 life insurance (temporary protection)

$28,430/year invested into non-registered account

This is what most people do: invest + temporary insurance

Strategy 2 (Daniel): Integrated Wealth Strategy

$750,000 permanent participating whole life insurance

$250,000 Term 20 rider

$4,918/year invested into non-registered account

This approach combines:

1) Tax-advantaged growth

2) Permanent protection

3)Access to capital during retirement

Outcome Over Time (After 20 years)

Michael’s portfolio: $1.9M (fully taxable growth)

Daniel’s portfolio: $1.32M + $1.5M+ life insurance benefit

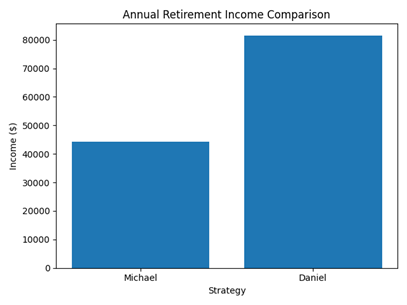

Retirement Income Comparison

Starting at age 65:

Michael: $44,214/year (interest-only withdrawals)

Daniel: $81,571/year

That’s 85% more income for Daniel

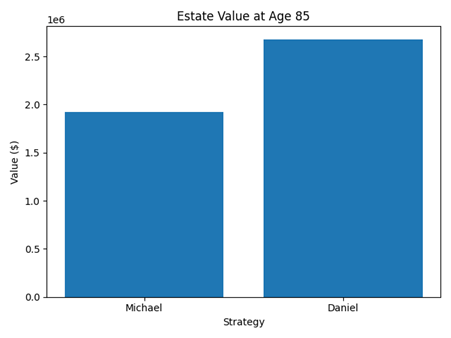

Long-Term Outcome (Age 85)

Michael’s estate: $1.9M

Daniel’s estate: $2.67M

40% higher estate value for Daniel

Why the Difference?

Daniel didn’t just invest, he repositioned part of his portfolio into a tax-efficient asset. This created:

Higher usable retirement income

Lower tax erosion over time

A significantly larger legacy

The Key Insight

This isn’t about choosing insurance vs investing. It’s about integrating both to improve outcomes. Most high-income earners focus on accumulation. But the real advantage comes from optimizing:

Tax efficiency

Income distribution

Estate transfer

If you’ve maxed out your registered accounts and still have capital sitting in taxable investments…

There may be a smarter way to:

Increase your retirement income

Reduce tax exposure

Leave more behind for your family

Ola Ofime

Ola Ofime is a licensed Investment and Insurance Advisor serving professionals, families, and business owners. Her expertise lies in helping professionals and business owners plan, invest, and secure their wealth

through tax-efficient financial strategies and insurance structures.

Follow me

ABOUT

Ola Ofime is a licensed Investment and Insurance Advisor serving professionals, families, and business owners.

QUICK LINKS

SUBSCRIBE

Created with ©systeme.io